The Missing Map to Financial Freedom Has Finally Arrived.

FreedomAtlas helps you make smarter financial decisions with personalized tools, a roadmap built for you, and your own Freedom Score™.

The Problem

Most people don't need more money.

They need better decisions.

People struggle because they're missing a roadmap. They don't know:

- ?How much to save right now

- ?Which debt to pay off first

- ?Whether they can afford that purchase

- ?How close they actually are to financial freedom

FreedomAtlas gives you clarity — one decision at a time.

Two people. Same income. Different decisions. Wildly different outcomes.

The Solution

Meet your personal Financial Operating System.

Personalized Guidance

Tailored recommendations that explain what to do next — and why.

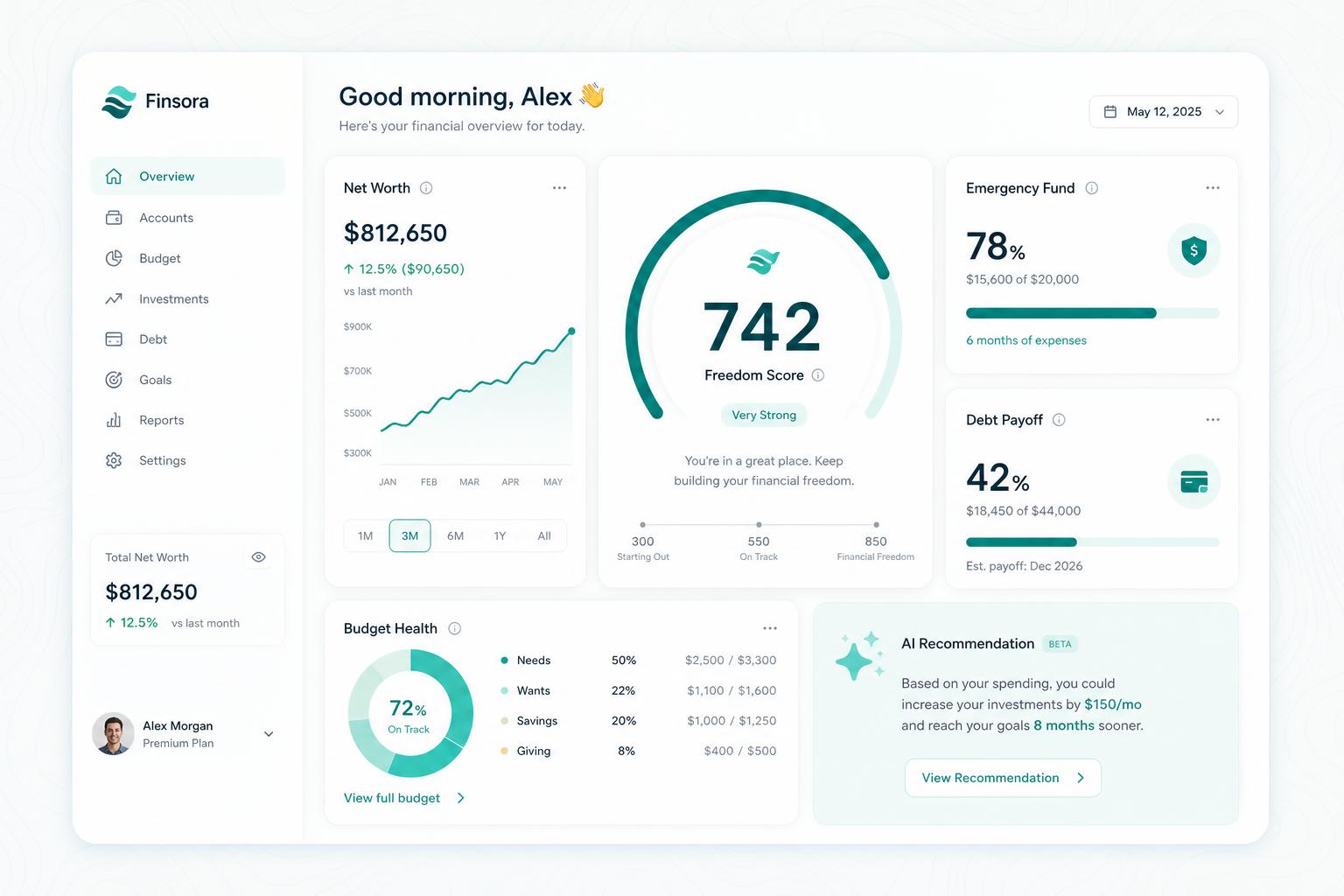

Freedom Score™

Track your financial progress with one simple number from 0 to 1000.

Digital Doors

Hundreds of calculators, planners, and decision tools, all connected.

Freedom Score™

Know your Freedom Score.

Your Freedom Score measures your financial readiness across ten key areas — and gives you a personalized roadmap for improvement.

Digital Doors

Every better decision starts with one Digital Door.

Emergency Fund Calculator

Find your safe cash cushion in under 60 seconds.

Budget Planner

Build a budget that actually fits your life.

Debt Snowball Planner

A payoff order that keeps momentum and morale high.

Net Worth Tracker

Know your real number — the truth in one screen.

Retirement Calculator

See if you're on track for the life you want later.

Compound Interest

Watch consistent investing become real wealth.

Mortgage Payoff

Years and interest saved by extra payments.

Savings Goal

Reverse-engineer any goal into a monthly number.

How it works

Three steps to a clearer financial life.

Answer a few questions

Takes about 3 minutes. No financial degree required. No bank linking.

Get your Freedom Score & personalized plan

We give you one number, ten pillar insights, and a custom roadmap.

Follow your roadmap

Open the right Digital Doors. Watch your score climb. One better decision at a time.

The Digital City

Hundreds of personalized tools. One connected platform.

Each neighborhood holds dozens of Digital Doors. Walk through any door, anytime.

Money

11 doors live

EnterHome

4 doors live · 16 more soon

EnterCareer

Coming soon

Business

Coming soon

Health

Coming soon

Family

Coming soon

Education

Coming soon

Travel

Coming soon

1,000+ Digital Doors coming.

Free download

Download the Financial Freedom Starter Kit.

Learn the seven steps to building lasting financial security — no fluff, no upsell.

What members are saying

Confidence. Clarity. Progress.

"For the first time, I have a single number that tells me how I'm actually doing — and exactly what to fix next. It's like Mint had a baby with a financial advisor."

"The Freedom Score moved me from anxious-about-money to in-control in about a week. I check it like I check the weather."

"I stopped guessing which debt to pay first, started the snowball, and watched my score climb 40 points in two months."

Free download

The Financial Freedom Starter Kit.

24 pages. Seven steps. Seven worksheets. The complete on-ramp to lasting financial security — free, forever.

The Financial Freedom Starter Kit

Seven steps to lasting financial security — with the worksheets to make each one real. Built from the same ten pillars we use in the Freedom Score.

Freedom Coach™

Meet your personal Freedom Coach™.

Ask anything. Get a grounded answer based on your real Freedom Score and Digital Door history — not generic advice from the internet.

Try Freedom Coach™Upgrade your journey.

Everything in free, plus the depth and tools serious decision-makers want.

See Premium- Unlimited Digital Doors

- Unlimited Freedom Coach™ conversations

- Family dashboard

- Saved calculations & scenarios

- Annual Freedom Report (PDF)

- Project planner

- Scenario comparison

- Freedom Timeline

- Priority access to new doors

Freedom isn't found.

It's built.

One better decision at a time.

Ready to build your freedom?

Join thousands of people making smarter financial decisions with FreedomAtlas.

FAQ

Frequently asked questions

What is FreedomAtlas?+

FreedomAtlas is a personal Financial Operating System. It combines hundreds of focused decision tools (Digital Doors), a personal Freedom Score, and a built-in Freedom Coach™ into one connected platform that helps you make better financial decisions.

Is it free?+

Yes. Every Digital Door is free to use, including your Freedom Score. FreedomAtlas+ unlocks unlimited Freedom Coach™ conversations, saved scenarios, a family dashboard, and an annual Freedom Report.

What is the Freedom Score?+

Your Freedom Score is a 0–1000 number that measures your financial readiness across 10 key pillars — emergency fund, budgeting, debt, net worth, investing, income, protection, home, planning, and habits.

Do I need to be good at finance?+

No. FreedomAtlas is built for normal people. Every tool asks plain-language questions and explains the answer in a way you can act on today.

Is my data private?+

Yes. Your inputs are private to your account. We never sell your data, ever.